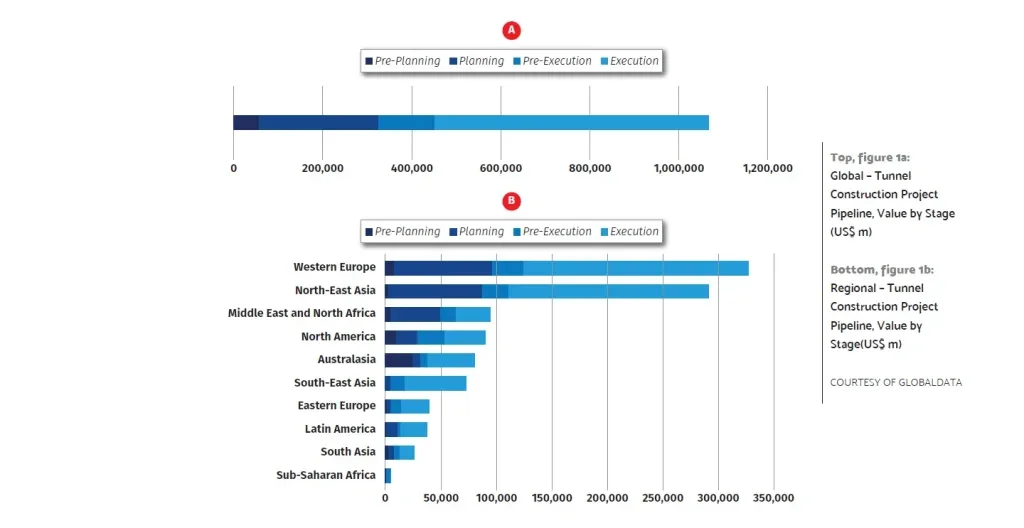

The latest data on tunnel projects globally show the value pipeline to be dominated by Western Europe and North-East Asia, and then the Americas – the combined total of North America and Latin America – is in third place, with approaching half as much.

The findings are in T&T sister publication GlobalData’s analysis for Q1-2024.

Within the Americas, the value pipeline in North America (US, Canada) is slightly more than double that of Latin America (which includes Mexico in the regional makeup for the analysis).

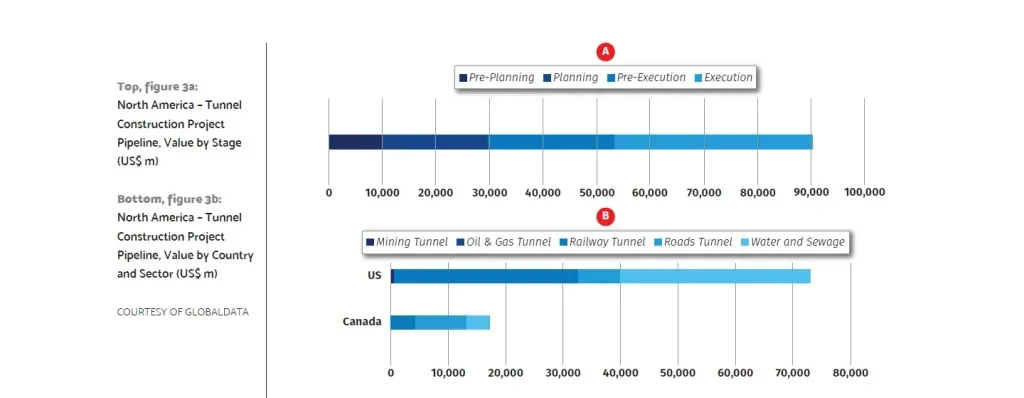

In terms of stage, the Execution phase is largest of the four stages (Pre-Planning, Planning, Pre-Execution, Execution) in North America’s value pipeline of tunnel projects; the Pre-Execution and Planning stages are almost comparable to each other, the former being slightly larger. Pre-Planning is the smallest stage by value, according to the analysis.

In terms of sectors, the project pipeline is led by Water & Sewage and Rail/Subway, respectively – especially in the US; in Canada they are, combined, comparable with tunnels for the road sector.

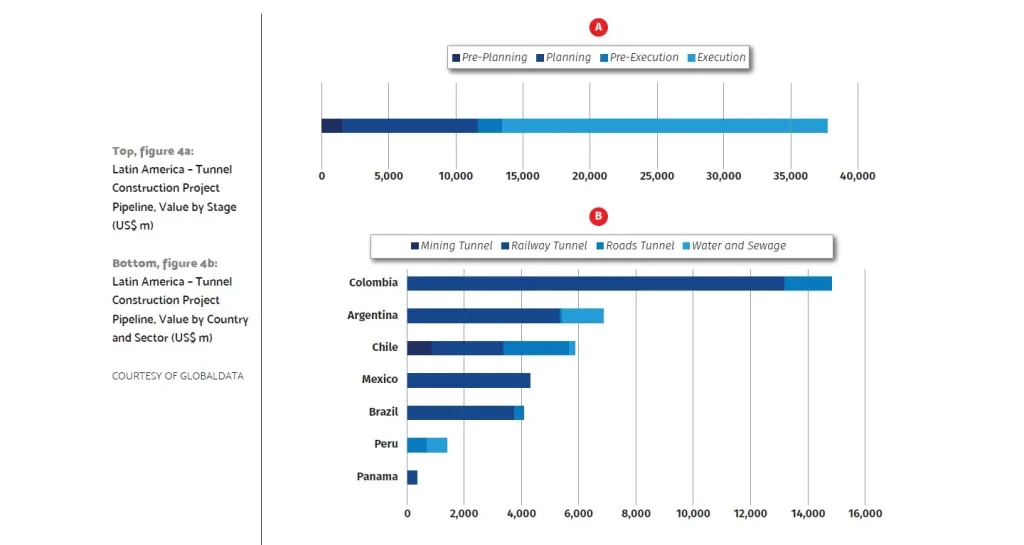

The project value pipeline in Latin America is markedly dominated by the Transport sector (primarily Rail/ Subway) with relatively little on Water & Sewage when compared to the proportion and scale in North America.

The nation that leads the project value pipeline in the region is Colombia – at more than double the levels of the nearest other countries (Argentina, Chile) in terms of pipeline value.

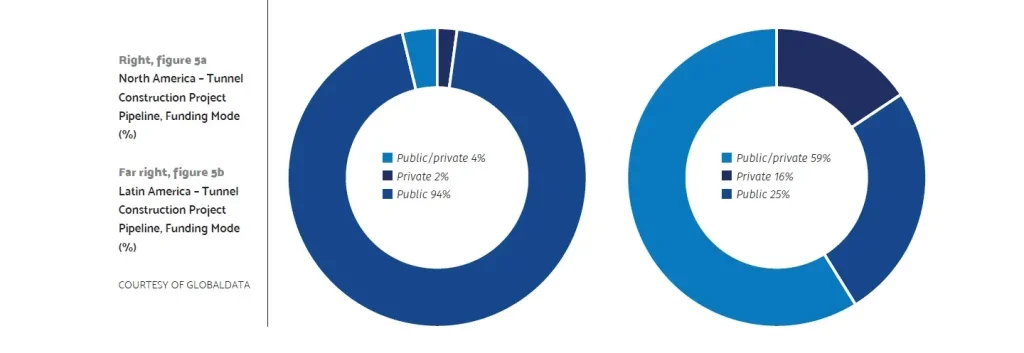

When it comes to funding modes of the tunnel construction pipeline the Americas also differ in their approach, but as a matter of degree: in North America the majority is by Public funding, leaving relatively little for the funding modes of Public/Private and Private, respectively; in Latin America the Public/Private and Private have proportionally more involvement while the overall picture is still dominated by Public funding.

With the global value pipeline of tunnel construction projects significantly led by Western Europe and North-East Asia (China, Japan mostly), it is noted by GlobalData that two North American projects make the list of Top 20 projects by value.

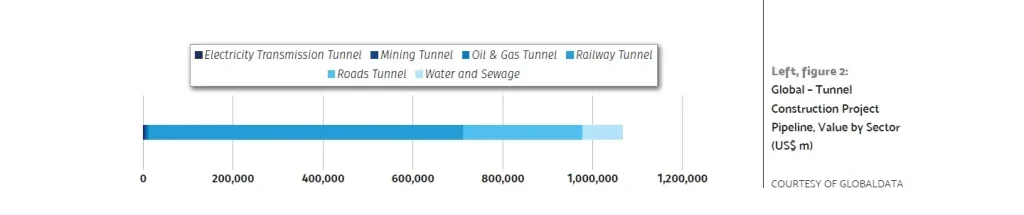

Globally, value pipeline of tunnel construction projects is primarily about Transport sector investment, with the focus on Rail/Subway by far. While Water & Sewage has a large share of the investment value in North America, in global terms it is minor by some way compared to the focus of the rest of the world on Transport.

The funding mode for the value pipeline of tunnel projects is dominated by Public funding. This is reflective of the share of Public funding for such investments in Latin America – and, as such, is proportionally smaller than the highly dominant role it plays in North America.

NORTH AMERICA

The tunnel construction project pipeline in North America totals approximately US$90 billion, and slightly more than a third of the sum (US$37 billion) is for projects in the Execution stage.

As noted previously, the value investment in the Pre-Execution and Planning stages are reasonably comparable (US$23.6 billion and US$19.7 billion, respectively) – and in combination they are more than the Execution stage. Currently in the Pre-Planning stage the tunnel project pipeline value across the region is slightly less than US$10 billion.

The North American tunnel projects pipeline, at present, shows a peak into 2025 then dips to even spending over 2027-28.

In terms of individual projects, the Top 20 by value in the region has 16 from the US and four from Canada – with three of the latter’s projects being in the Top 10

US

With the US market by far the larger of the two countries in North America in the analysis (US, Canada), the relative shares of the country’s total value pipeline by tunnel project stages (US$73 billion) reflects those of the whole region. The Execution stage pipeline is, by value, the largest (US$31.6 billion); next is Planning, very closely followed by Pre-Execution; the Pre-Planning stage is smallest by value.

The project pipeline is led by two sectors that are almost equal in size – Water & Sewage and Rail/ Subway, respectively. With the addition of the relatively small Road sector to the far larger Rail activity, the Transport sector as a whole is then the main area of infrastructure development in the US tunnel pipeline

Canada

In the Canadian market, there is currently a fairly even split between three of the total value pipeline (US$17 billion) by tunnel project stages – Pre-Planning, Pre- Execution, and Execution. At present, the smallest of the stages by value pipeline is the Planning stage.

The tunnel value project pipeline is led by the Road sector, accounting for approximately half of the total. When combined with Rail, the total for Transport equates to about three-quarters of the total.

LATIN AMERICA

As noted above, the tunnel project value pipeline in Latin America is markedly dominated by the Transport sector (primarily Rail/Subway) with relatively little on Water & Sewage, and nationally by Colombia.

In terms of stage, GlobalData says the value of the Latin American pipeline is weighted towards projects in the later stages of development. With respect to tunnel length, as tracked by GlobalData, it adds that the Latin American pipeline is comprised of just over 250km of tunnel projects, the largest share in Chile, followed – and in a close-tie – by Colombia and Argentina.

GlobalData says Colombia records the highest value pipeline of tunnel construction projects in Latin America, accounting for about 39% of regional project value.

It adds that tunnel construction in the country will be driven by government investment in infrastructure and the development of the new fifth-generation series of infrastructure projects.

The country has one of the biggest tunnel projects in the region – Bogota subway, which is part of a larger transport masterplan.

QUARTERLY REPORT: PROJECT INSIGHT – GLOBAL TUNNEL CONSTRUCTION PROJECTS. Q1-2024

From GlobalData, a T&T sister publication. GlobalData is a leading provider of data, analytics and insights on the world’s largest industries, including construction, and sectors such as transport (road, rail) and water & wastewater. www.globaldata.com