As reported previously in T&TI, analysis is showing that government budget are squeezed enough to results in short-term reduction in budgets for infrastructure, including those with tunnels to greater or lesser degree. Pressures are within the economies of nations and across borders, leading to reduced plans in many regions, although somewhat less so in the US, China and India.

Even so, much is either in the development pipeline or already underway for the dominant sector of infrastructure – transport, including projects with tunnels. Within Transport the leader is Rail & Metro.

GlobalData’s latest tracked data, for the third quarter-2024 (Q3-’24), the pipeline of tunnel projects worldwide across all sectors – that is, construction work underway or planned that contains some portion of underground works – is approximately US$1 trillion. This value pipeline is therefore not for only underground works but where tunnels make up a notable or large share of the project investment across the sectors, including Transport.

Such infrastructure projects, range across the full spectrum of phases of development, from those in early planning or design activity to others that have entered into construction procurement or where works are already on site, either in initial, mid or advanced stages. There is much in the initial (planning and design) stages, but more than half of the value pipeline is for tunnelrelated projects already in construction, according to GlobalData’s Q3-’24 analysis.

On a different measure – total distance being built – most of the infrastructure projects with tunnels (in greater or lesser portion) are in Western Europe, Middle East and North Africa (MENA), and North America. Together, they have approximately two-thirds of the total.

In terms of the Transport sector though, and in particular Rail & Metro, the regions with most activity continue to be – as per prior GlobalData analysis (Q1-’23) – Western Europe (Germany and Alpine nations, and UK) and Northeast Asia (primarily China and Japan).

In terms of an overview on funding, most tunnelrelated projects (81%, globally) are publicly funded, varying from 60% to 90% of pipeline investments across the regions analysed by GlobalData.

There is use of public/private funding although globally it takes only a relatively minor share (14%) – apart from Latin America where it accounts for more than half of the region’s funding, and in MENA, Eastern Europe, Western Europe, Australasia, and parts of Asia, respectively, where the mode holds double-digit percentages. Least used, globally, is the private funding mode (5%) and which is only present in some regions, and where it is used most is Latin America (16% of the regional funding) and Western Europe (13%).

As noted earlier, most of the total pipeline of investment in tunnel-related projects relates to the transport sector – in fact 91%, according to GlobalData’s Q3-’24 analysis. Within Transport, spend on the Rail & Metro is largest, on an approximately 3:1 ratio compared to Highways & Roads.

EUROPE

Western Europe

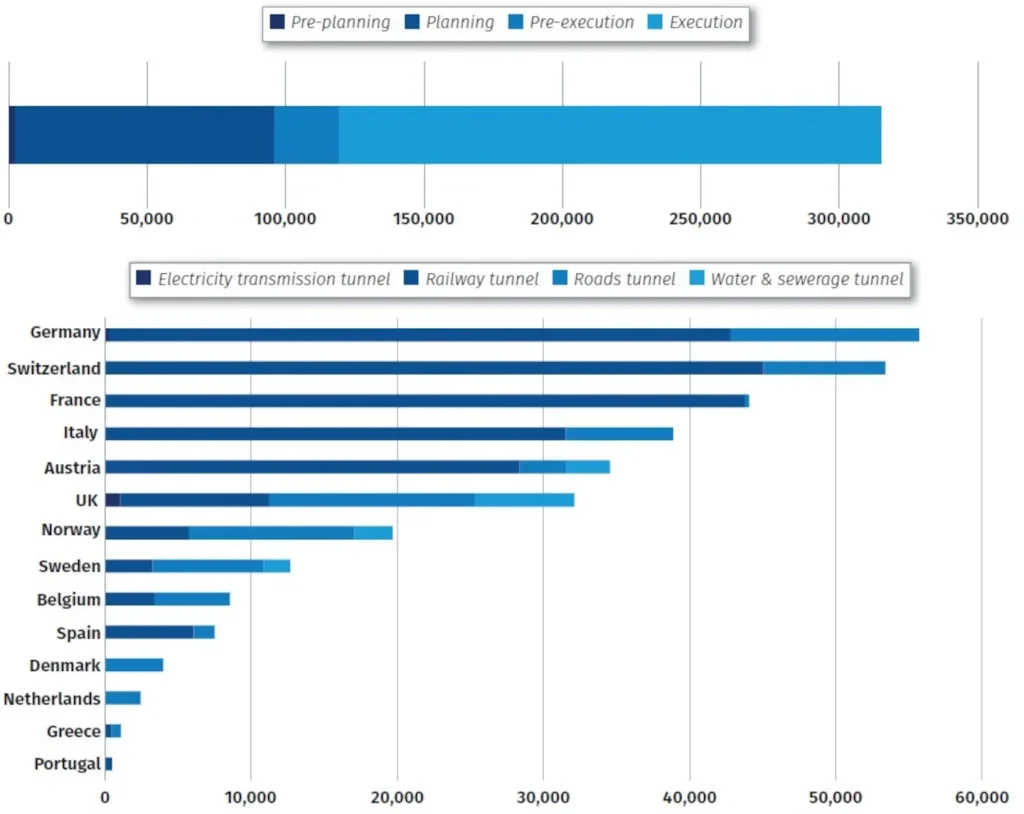

The region had a value pipeline in total tunnel-related construction projects of about US$315 billion, led by investments in Germany, Switzerland, France, Italy, Austria and UK, with projects also in Norway, Sweden, Belgium and Spain.

Most of the regional pipeline is for tunnel-related projects in pre-execution and execution phases.

Rail & Metro activity (across all phases) in the region is approximately US$221 billion and almost three times as large, by value, as Highways & Roads.

By nation, the tunnels-related Rail & Metro activity is led, in ranked size, by Switzerland, France, Germany, Italy and Austria.

The first three are almost tied, as are the last two. Other Western European nations have much less Rail & Metro investment, relatively, and for those there is a switchover in Transport investment to favour Highways & Roads tunnel-related projects.

Eastern Europe

The total tunnel-related construction pipeline in Eastern Europe is about US$40 billion, with national activity led by Romania, Turkey and Poland. Public funding (80%) of projects is by far the leading mode in this region, although public/private is a high share (19%).

Rail & Metro’s share of the total – and therefore Transport sector – value pipeline is dominant in the region, and this comes from high activities in Romania, Turkey and Poland.

Roads tunnel projects feature only in a very minor way in the region, according to the analysis. What activity there is takes place, primarily, in other countries such as Bosnia & Herzegovina, Bulgaria, Georgia, and with some in Turkey.

Kazakhstan is different – it tunnel-related infrastructure is primarily to serve resource and energy extraction industries – mining (copper, uranium) and oil & gas, respectively.

ASIA

Northeast Asia

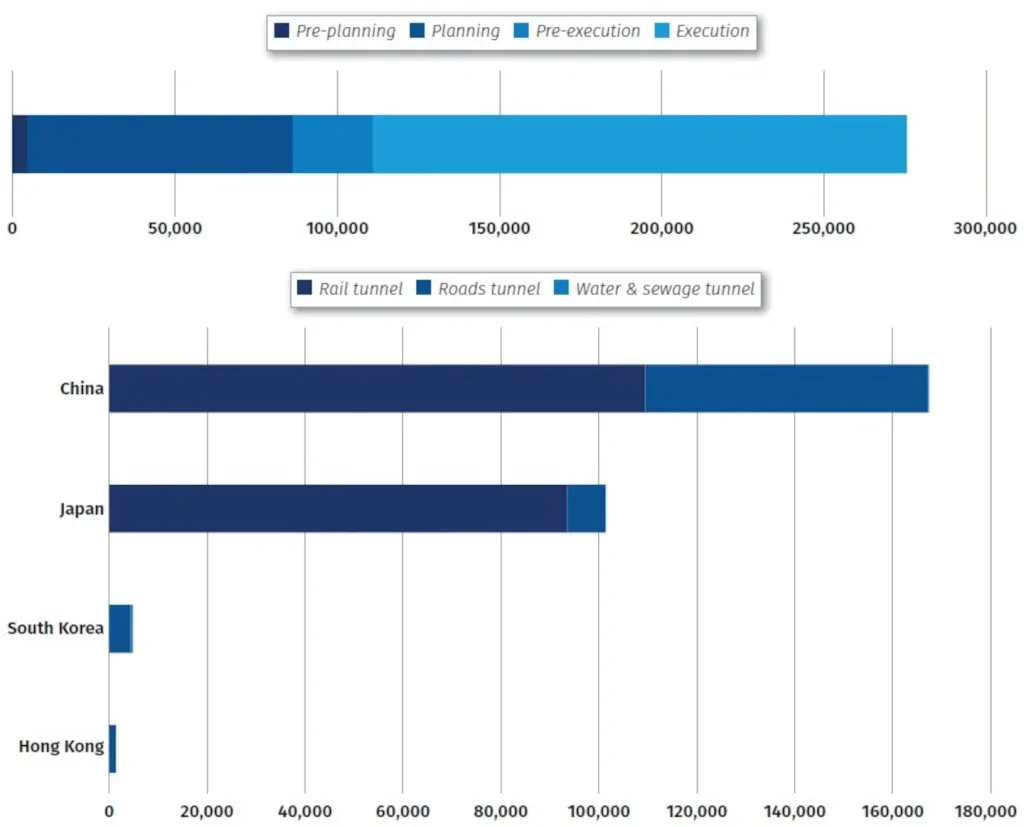

The total tunnel-related construction pipeline in Northeast Asia is about US$275 billion, dominated by Transport investment in China and Japan. The value pipelines in those two counties far outweigh the tunnelrelated project activities elsewhere in the region, in South Korea and Hong Kong by large measure.

Rail & Metro investment in tunnels-related projects accounts for the majority of Transport sector, and all tunnel activities in the region. The value pipeline for Rail & Metro’s tunnel-related projects is US$203 billion, according to the latest GlobalData analysis, and much larger than the US$72 billion for Highways & Roads.

The Rail & Metro value pipeline is almost in balance between China and Japan, although in the latter it is almost completely the total spend. With proportionally, and in value, more spend on Highways & Roads in China the country still has investment led by Rail & Metro, accounting for about two-thirds of the national total.

Across all sectors, most of the tunnels-related projects in the region are publicly funded (89%) although with public/private mode holding a not insignificant share (11%).

Southeast Asia

The total tunnel-related construction pipeline in Southeast Asia is about US$73 billion, notably led by Singapore, and then Malaysia, Thailand, Indonesia and Vietnam.

Regionally, the largest share of activity stage for the projects is pre-execution and execution, and this is reflected in the largest activity nations – Singapore and Malaysia. Pre-planning and/or planning only feature, and in small ways, for data listed for Indonesia and Thailand. More stages of Singapore metro are to come but weren’t showing in the categories.

In terms of tunnel-related Roads & Metro projects, this sub-sector is dominant in the region, and in – and by virtue of – Singapore’s value pipeline. In total the region has US$55 billion of Rail & Metro activity in tunnels-related projects, followed some way behind by Highways & Roads, at US$10 billion.

On funding, the analysis puts the modes and their shares at the same types and levels as for Northeast Asia – public (89%) and public/private (11%).

South Asia

The total tunnel-related construction pipeline in South Asia is about US$24 billion. The region comprises – ranked in decreasing order of total tunnel-related project pipeline value – India, being larger by multiples over the following main nations spending which are Nepal and Pakistan.

About one-third of the total pipeline activity of tunnel-related infrastructure projects in the region is pre-planning and planning stages of development, in total; the majority in pre-execution and execution phases.

Tunnel-related Highways & Roads projects feature most in investments in this entire region – particularly so in India (although it has many Rail & Metro developments) but also in Nepal and Bangladesh. The Transport pipeline in India is just over US$14 billion, which is more than half of all tunnel-related activities in the entire region. Of that sum in India, about one-eighth relates to Rail & Metro.

Early stages of project development (pre-planning and planning) have a bigger share of activities in India; the other nations, while their overall investment pipelines are much smaller those activity stages, have projects that are more weighted toward execution phases.

Most of the projects in the region are publicly funded (87%), with public/private (12%) having no small role but private (1%) being small.

AMERICAS

North America

The total tunnel-related construction pipeline in North America is about US$87 billion. The region comprises the US and Canada, the former value pipeline being proportionately larger than the latter by a ratio of 4:1.

However, despite the difference in scale nationally, the large scale of water & sewerage tunnel projects in the US takes up much of the share of value, proportionately far more than in Canada. This results in the total value of tunnel-related transport projects in the US being only 3:1 larger than in Canada.

In the US, by far the most investment in tunnel-related Transport projects is in Rail & Metro, slightly edging out the relatively large spend (compared to many other nations, and regions) on Water & Sewerage.

In Canada, Highways & Roads projects dominate all sector activity, although key Rail & Metro projects are underway in cities like Toronto.

By far the majority of the region’s project pipeline is publicly funded (97%), then private (2%) and public/ private (1%).

Latin America

The total tunnel-related construction pipeline in Latin America is about US$31 billion. The region mostly comprises – ranked in decreasing order of total tunnelrelated project pipeline value – Colombia, Chile, Mexico, Brazil, Argentina and Peru.

Once again, the Rail & Metro value pipeline holds sway in a region, and the most active countries in the sub-sector are Colombia, Mexico, Brazil and Chile, in decreasing order. Colombia leads by far – the Rail & Metro spend being more than the rest combined. The investment is seeing much development in the region’s major cities, leaving only a minor share of activity in Highways & Roads.

Unlike other regions, overall in the tunnel-related construction pipeline, in Latin America the dominant mode is public/private mode (59%), followed by public (25%), then private (16%).

AUSTRALASIA

The total tunnel-related construction pipeline in Australasia is about US$63 billion. The region comprises New Zealand and Australia, the latter value being about 70% of the former. Overall, the region has pre-execution and execution stage activities that slightly outweigh those in pre-planning and planning.

The tunnels-related Rail & Metro projects are, by far, the majority of activities in both countries. There is little underway, relatively, on Highways & Roads. In total, the value pipeline in Rail & Metro is more than eight times bigger than Highways & Roads.

In funding, most projects are publicly funded (86%) with public/private mode accounting for the rest (14%).

MIDDLE EAST & NORTH AFRICA (MENA)

The total tunnel-related construction pipeline in MENA is about US$93 billion with total tunnel-related project pipeline value led by Israel and Iran. Most of the projects are publicly funded (74%), then public/private (23%) and private (3%).

Most pipeline activity in the region is though, once again, dominated by Rail & Metro projects. The sub-sector of transport constitutes almost all of the pipeline in Israel, and about-three-quarters of tunnels investment in Iran, according to the analysis.